If you have to retire early from your main occupation perhaps because of ill health or redundancy, you may have to review your retirement plans. There are a number of actions you could consider.

What if I have to retire early?

Use other savings and investments

Any savings and investments can help boost your income, often tax-efficiently.

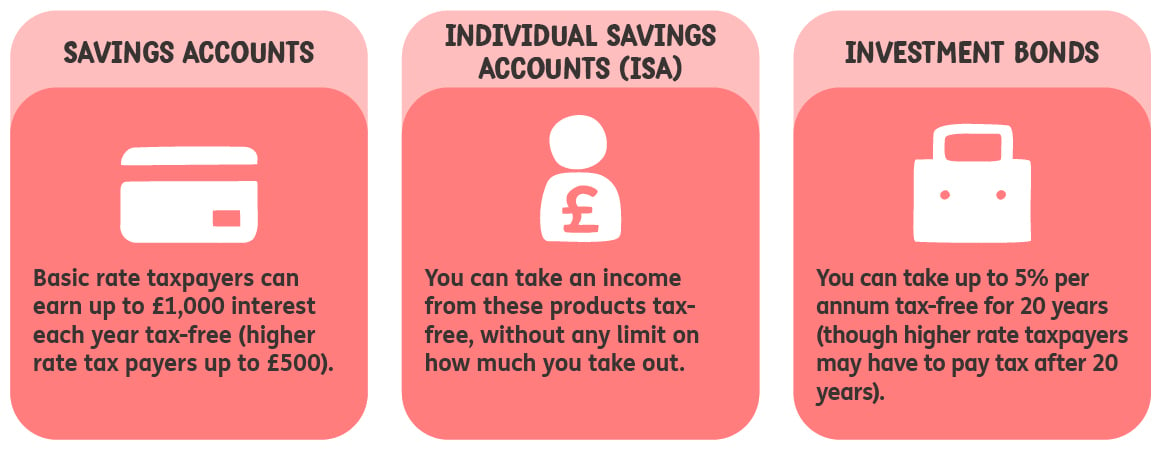

Increasingly, people rely on other savings and investments they have to support their life after work. What’s more, many of these products can pay an income free of tax. Here are some examples:

If you invest in stocks and shares directly or through a product – usually a unit trust, open-ended investment company or investment trust – you can withdraw up to the Capital Gains Tax Allowance each year without paying any tax. The Capital Gains Tax Allowance is currently £3,000 (2024-25).

Releasing equity from your home

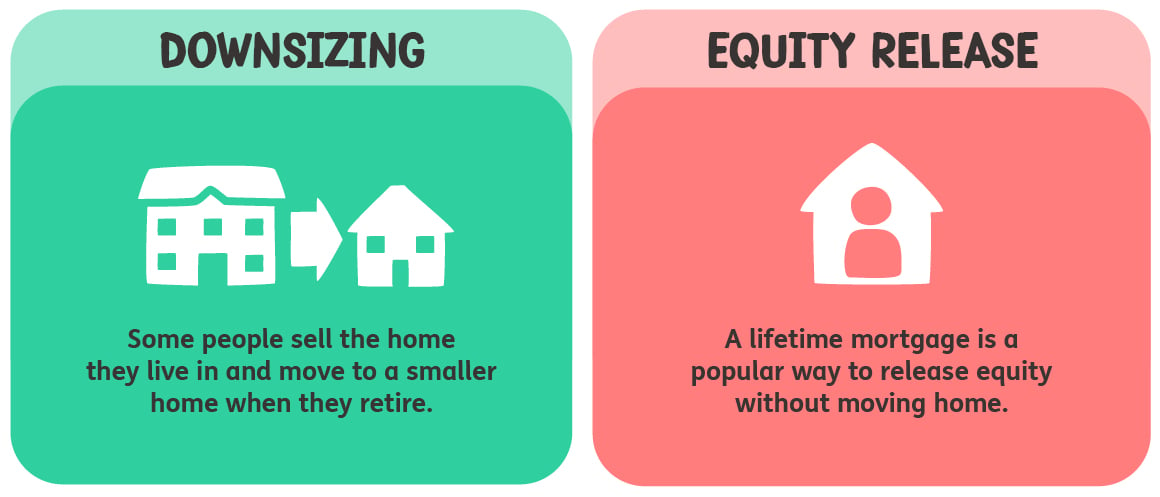

The equity in your home is often your greatest asset.

Your home can be a valuable source of income to support your life after work. There are different ways to do this.

The two main options are:

Downsizing could be the right course, but there are also things to consider:

• You may still need spare bedrooms for grandchildren to stay, so don’t overdo it.

• There will be costs in buying and selling. Make sure you release enough equity.

• When the time comes, it can be emotionally difficult to sell the family home.

If you take a lifetime mortgage, which is a type of loan secured against your home, there are a number of issues to consider. For example:

• It will reduce the amount you could otherwise leave to your loved ones.

• Interest rates are often higher than those payable on conventional mortgages.

• If you choose not to make regular interest repayments during the life of the loan, the amount you owe can grow rapidly.

To read more on this subject check out our Pension Buddy Guide to Other sources of income in retirement

Review your spending

You’ll often find there are savings to be made if you look closely.

Create a budget for retirement. Start by looking at your bank statements to understand your current spending. Then make some adjustments:

• Think about what expenses will reduce or disappear in retirement. Will you have paid off your mortgage? Will you no longer need to commute? Perhaps you’ll spend less on clothes and take fewer expensive holidays?

• In contrast, what might you spend more on in retirement? Energy bills could increase if you’re at home most of the day. Maybe you’ll spend more money on hobbies and interests?

• Split spending between essential expenses, important expenses and optional expenses. If you need to make cuts, you can start with optional expenses first.

Other expenses

Some of your expenditure won't occur each month or even each year.

Once you’ve completed your budget ask yourself:

• Where could I make cuts? Review your optional expenses. Do you need to dine out so much each month or take as many holidays? You may not be prepared to compromise on this spending, but take a thorough look at where cuts could be made.

• Can I get better deals? Check out the costs of insurances on your car and home. Are there cheaper deals available elsewhere? How about your internet and energy providers? Could you save money by switching suppliers?

Can I take more income?

You may be able to take more income from your pension, but care is needed.

If you decide to convert your pension pot into income using drawdown, you choose how much income to take each year.

If you want an income that should last a lifetime, and increases each year to offset inflation, some research suggests taking between 2-4% of your pension pot each year. This is based on someone retiring at 65.

These figures aren’t guarantees, but an indication of the level of income you could take to try to avoid running out of money.

There are circumstances when you could consider taking more than 2-4% each year. For example:

• Poor health. If you suffer from a medical condition likely to significantly shorten your life expectancy you could consider taking a higher income.

• Other assets. If you have other savings and investments to fall back on, or if you’re prepared to release equity from your home, you could take perhaps more income

• Ignore inflation. If you choose a fixed income that doesn’t increase each year you could take a higher income. Expenses often fall during retirement so this can make sense.

• If you’re much older than 65 when you retire. Your savings don’t need to last as long, so you could take more than 2-4% each year.

Taking more than 2-4% each year is a risk. Even if you suffer from poor health you could still live longer than expected. Alternatively, if inflation is much higher than predicted, it could significantly reduce the spending power of your money in future. For example, in 2008 a pint of beer cost £2.30 and a fish supper £2.43! And if your investments don’t perform as expected this can also impact how much income you can safely take.

If in doubt, think about taking professional financial advice.

"Drawdown"

Drawdown means your pension savings stay invested, just like when you were saving for retirement. You can take income by simply selling part of your investments when you need money. You can withdraw what you want, when you want. This makes drawdown very flexible, but your income isn't guaranteed and you could run out of money.

Working after retirement

Over one million people still work past their 65th birthday.

Increasingly people retire from their main occupation, but still work in some capacity. If you’ve been made redundant, this might be a possibility. It could be more difficult if you’ve retired early through ill health, but there may jobs you could still consider.

At the same time, there are a few pitfalls to be aware of.

• Means-tested benefits. If you are receiving or expect to receive means-tested benefits such as Pension Credit, Housing Benefit or Council Tax Support, the amount you’re entitled to could be affected if you work beyond retirement.

• Higher tax band. If you continue working, but also take your State pension and/or any private pension, this may tip you into a higher tax bracket.

You may also be interested in...

Using your pension savings

There are a number of options available