You may be able to take more income from your pension, but care is needed.

If you want an income that should last a lifetime, and increases to offset inflation each year, some research suggests taking around 2-4% of your pension pot each year. This is based on someone retiring at 65.

These figures aren’t guarantees, but an indication of the level of income you could take to try to avoid running out of money.

There are circumstances when you could consider taking more than 2-4% each year. For example:

• Poor health. If you suffer from a medical condition likely to significantly shorten your life expectancy you could think about taking a higher income.

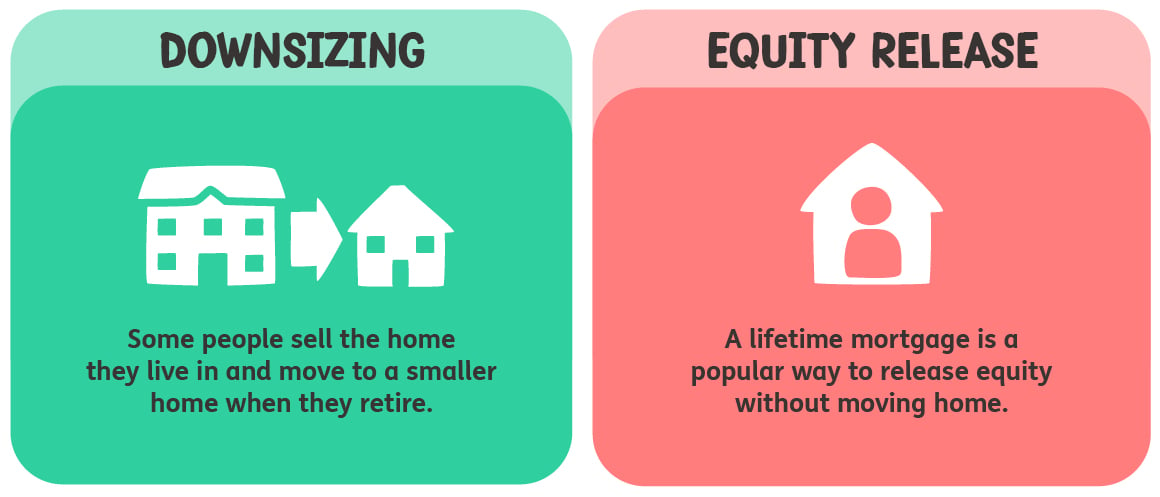

• Other assets. If you have other savings and investments to fall back on, or if you’re prepared to release equity from your home, you could take more income.

• Ignore inflation. If you choose a fixed income that doesn’t increase each year you could take a higher income. Expenses often fall during retirement so this can make sense.

• If you’re much older than 65 when you retire. Your savings don’t need to last as long, so you could take more than 2-4% each year.

Taking more than 2-4% each year is a risk. Even if you suffer from poor health you could still live longer than expected. Alternatively, if inflation is much higher than predicted, it could significantly reduce the spending power of your money in future. For example, in 2008 a pint of beer cost £2.30 and a fish supper £2.43! And if your investments don’t perform as expected this can also impact how much income you can safely take.